The Signal: May 2025

![]()

By Chris Davis | July 31, 2025

May 2025 has become a reference point for the post-pandemic recalibration of the business travel sector. With the timing of Easter holidays reverting to April, May offered a rare clean comparison with the previous year, but the results exposed persistent headwinds facing the U.S. corporate travel market.

Significant Declines in Corporate Air Travel

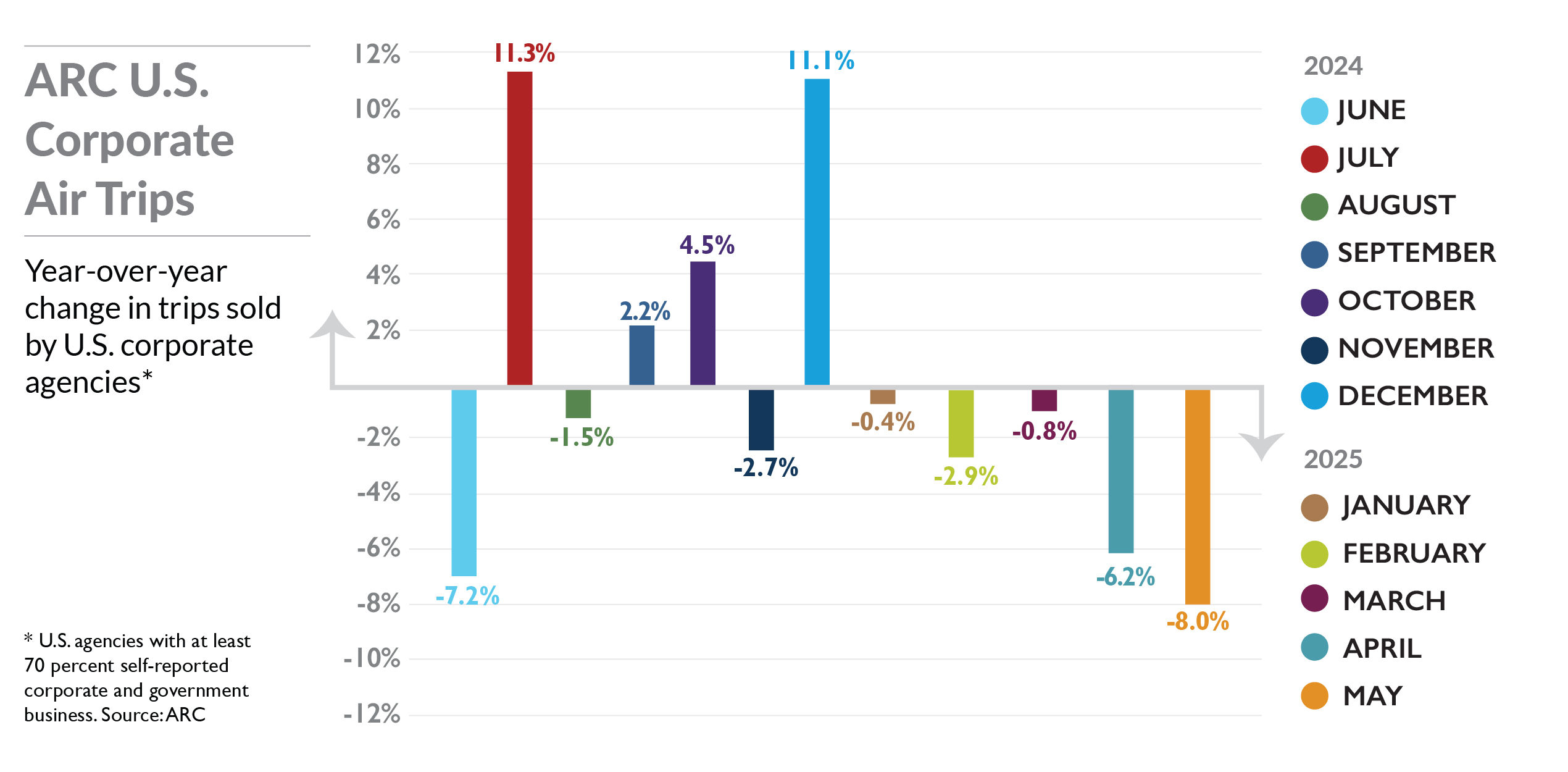

According to data released by the Airlines Reporting Corporation (ARC), U.S. corporate travel agencies sold 8% fewer air tickets in May 2025 than in the same month the previous year. This marks the fifth consecutive month of year-over-year declines and is the steepest drop since the COVID-19 pandemic severely curtailed global travel in 2020.

This contraction follows a period of recovery in 2023 and early 2024, and analysts attribute the softness to a mix of economic uncertainty and geopolitical developments—most notably, the Trump administration’s ‘Liberation Day’ tariffs, which were implemented and later partially rolled back amid international pushback and domestic business concern. These trade measures have been blamed for contributing to a climate of hesitancy among corporate travel buyers, with some companies imposing new restrictions or deferring non-essential trips.

Domestic Versus International Trends

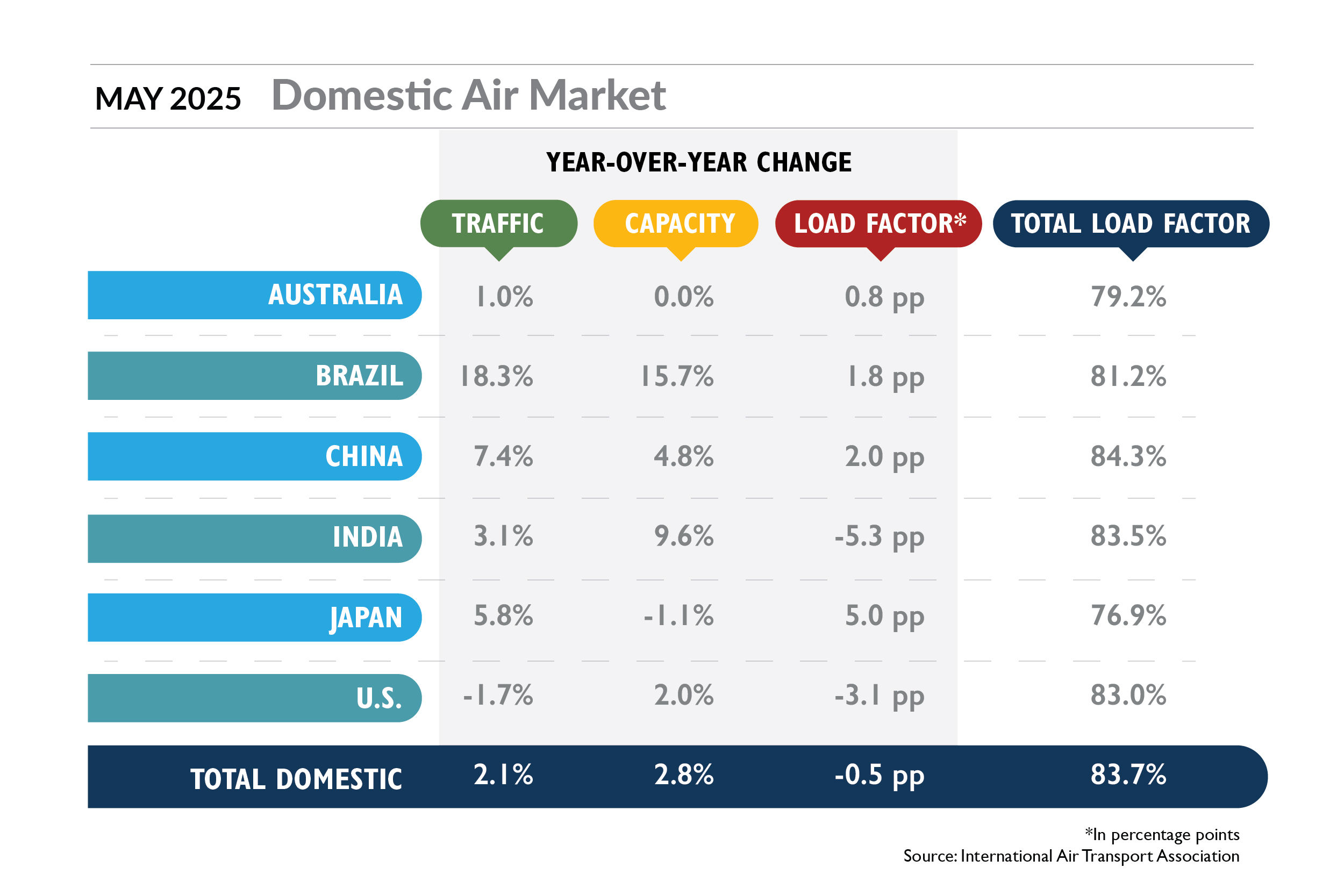

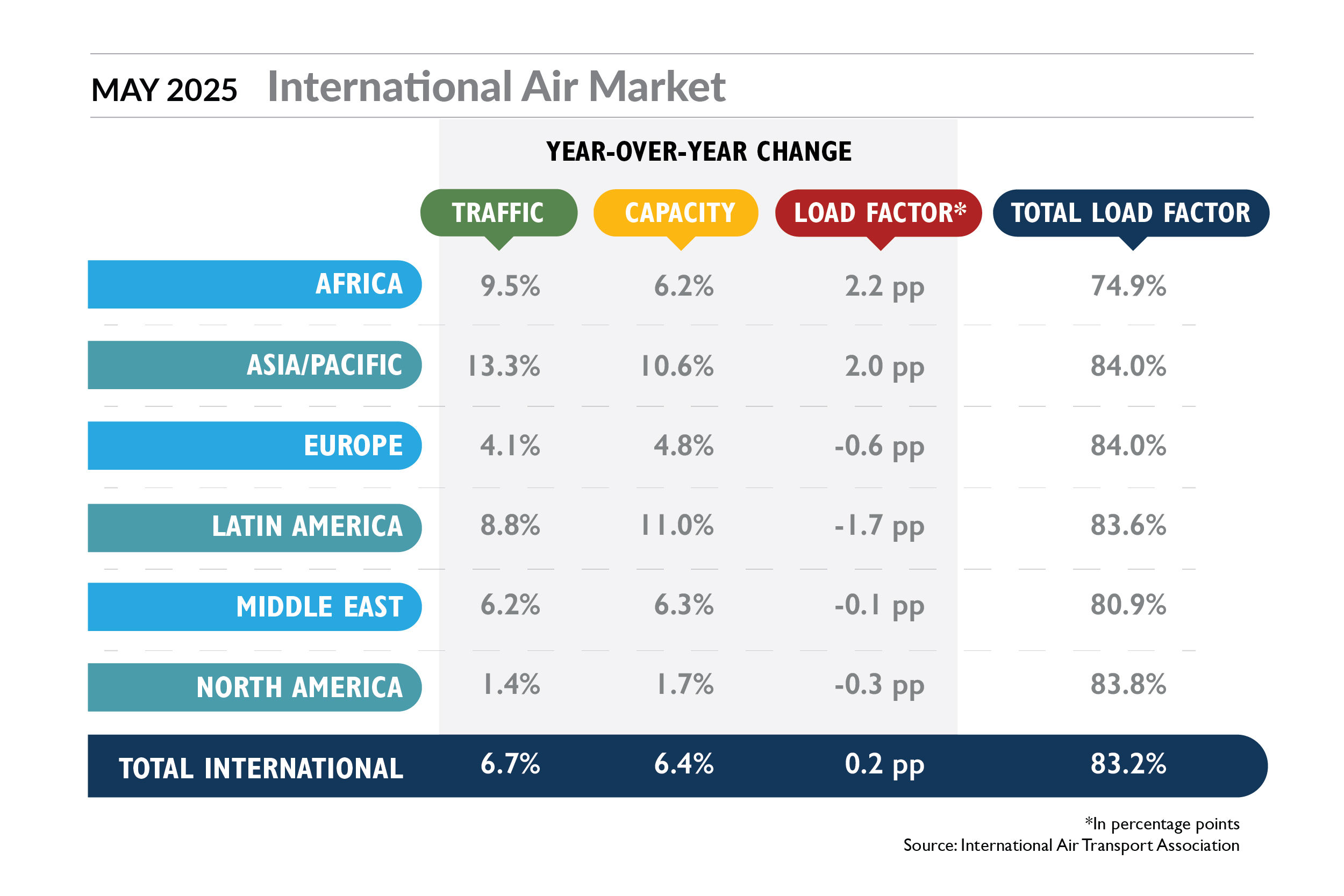

The International Air Transport Association (IATA) reported that U.S. domestic air demand, measured by revenue passenger kilometers, fell by 1.7% year over year in May—marking four consecutive months of decline. In contrast, international air travel demand across all regions was up 6.7% year over year, highlighting a growing disparity between subdued U.S. corporate activity and robust international appetite for travel.

IATA’s Director General, Willie Walsh, commented, “Air travel demand growth was uneven in May. Importantly, consumer confidence appears to be strong with forward bookings for the peak Northern summer travel season, giving good reason for optimism.” Indeed, outside North America, no other major market tracked by IATA reported declines in domestic travel.

Changing Ticket Pricing and Corporate Buying Trends

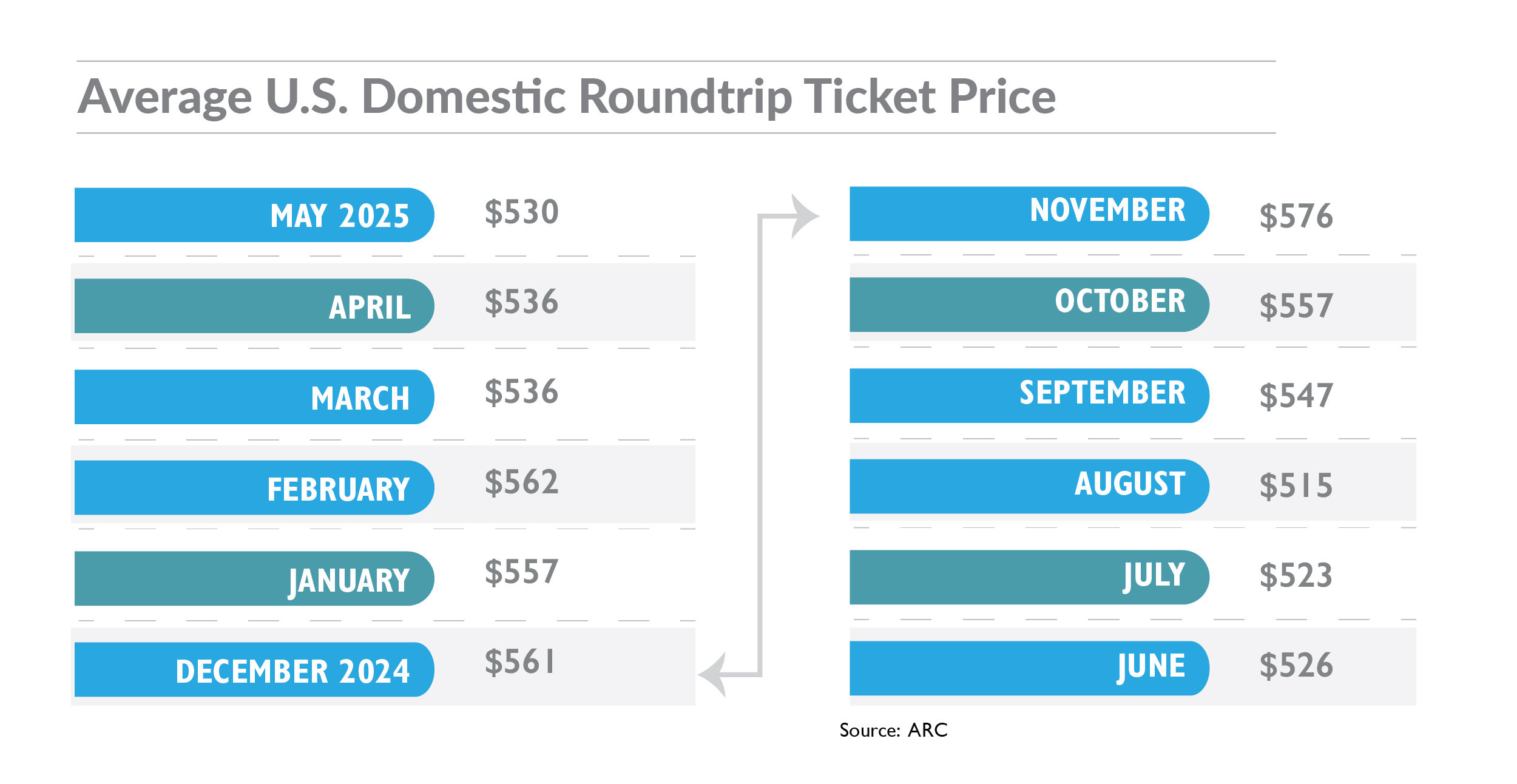

Despite decreased demand, the overall average U.S. domestic ticket price in May fell to its lowest point since August 2024. However, ARC data show that premium ticket prices actually increased by about 2% year over year, indicating continued demand for flexibility and upscale service tiers among corporate travelers who do travel.

These pricing patterns reflect an ongoing recalibration in business travel procurement. Many organizations have adopted stricter travel approval processes and increased use of virtual meeting technologies, resulting in fewer—but more essential—business trips. When travel is approved, it is often for high-value meetings, partially explaining the resilience in premium cabin demand.

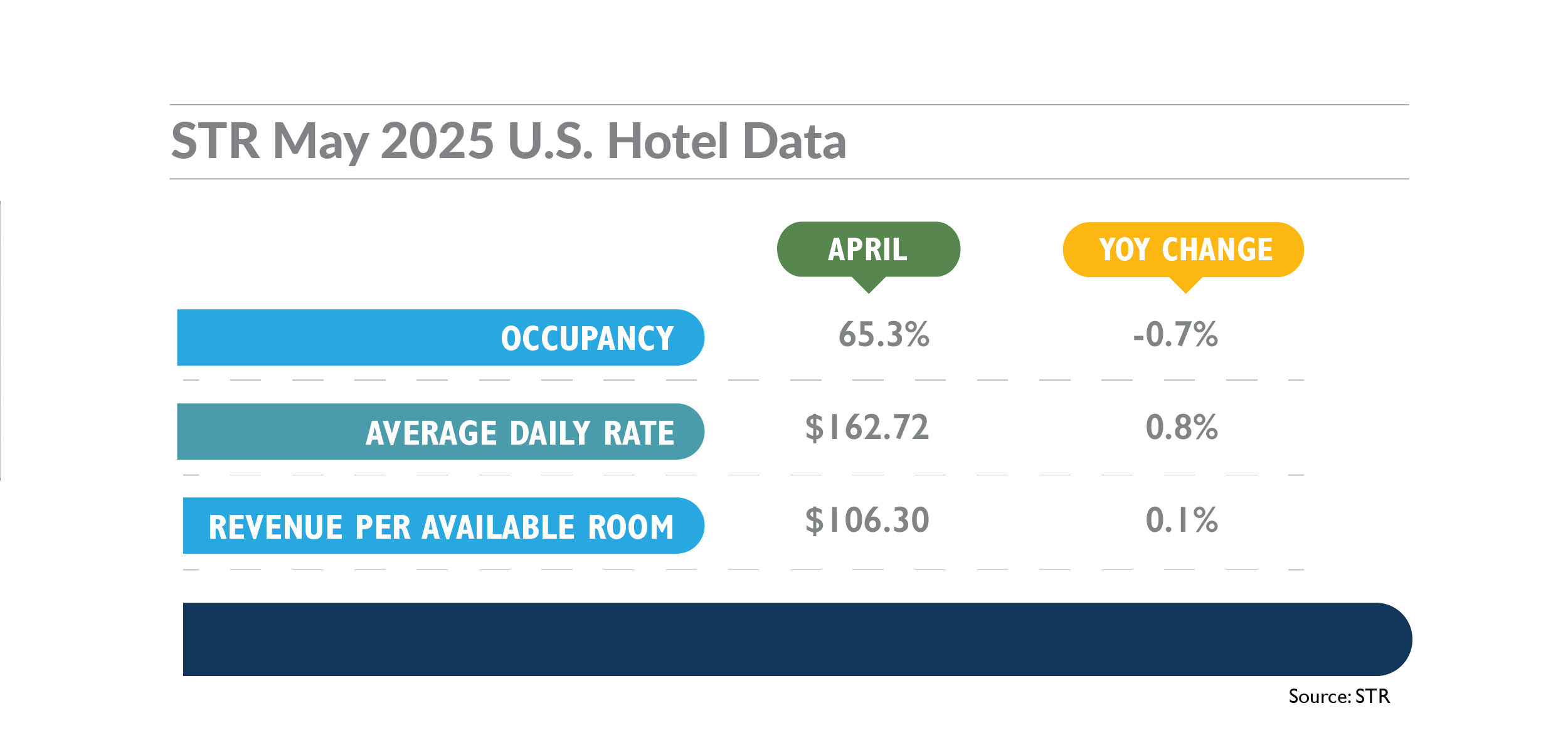

U.S. Hotel Sector Mirrors Air Travel Challenges

The hospitality industry also saw a noticeable shift in May 2025. Data from hospitality analytics firm STR reveals U.S. hotel occupancy rates fell year over year for the third consecutive month, nullifying the previous stretch of growth and introducing new cautionary signals for hoteliers and investors. Despite the occupancy drop, average daily rates (ADR) crept higher, suggesting some properties successfully maintained pricing power despite softer demand.

The dip in hotel performance echoes the pandemic-era trend toward shorter booking windows and increased volatility in group bookings, both influenced by cautious corporate clients and late-breaking meetings or cancellations. Larger urban markets like New York, Chicago, and San Francisco reported sharper declines than secondary business destinations, reflecting the continuing transition in corporate headquarters and event strategies.

Global Context and Forward Outlook

The North American retreat in business travel comes amid a broader global rebound. International demand continues to surge as Asia-Pacific and European markets regain pre-pandemic momentum, driven by improved border access, continued digital transformation, and growing investor confidence in global supply chains. The World Travel & Tourism Council projects global business travel spending will reach $1.4 trillion by the end of 2025, but warns that North America’s lag will weigh on overall rates of growth.

Corporate travel managers are cautiously optimistic for the latter half of 2025, noting strong advance bookings for major conferences and industry events coinciding with the summer season. However, continued geopolitical uncertainty, inflationary pressures, and technology-driven meeting alternatives will influence how and when organizations resume a steady pace of business travel.

{kind=link}