Weekly Market Wrap: AI Fuels Summer Gains as Rate Cuts Loom, Volatility Ahead

Published: August 29, 2025

Author: Angelo Kourkafas, CFA

Summer Heats Up as AI and Rate Cut Hopes Energize Markets

As the final days of summer pass, U.S. equity markets remain buoyant, notching a fourth consecutive month of gains in August. This bullish performance has been powered largely by ongoing enthusiasm for artificial intelligence (AI) and shifting expectations that the Federal Reserve may soon begin cutting interest rates. Against a backdrop of a fundamentally resilient U.S. economy, investors must now navigate the seasonally volatile autumn months with strategic discipline.

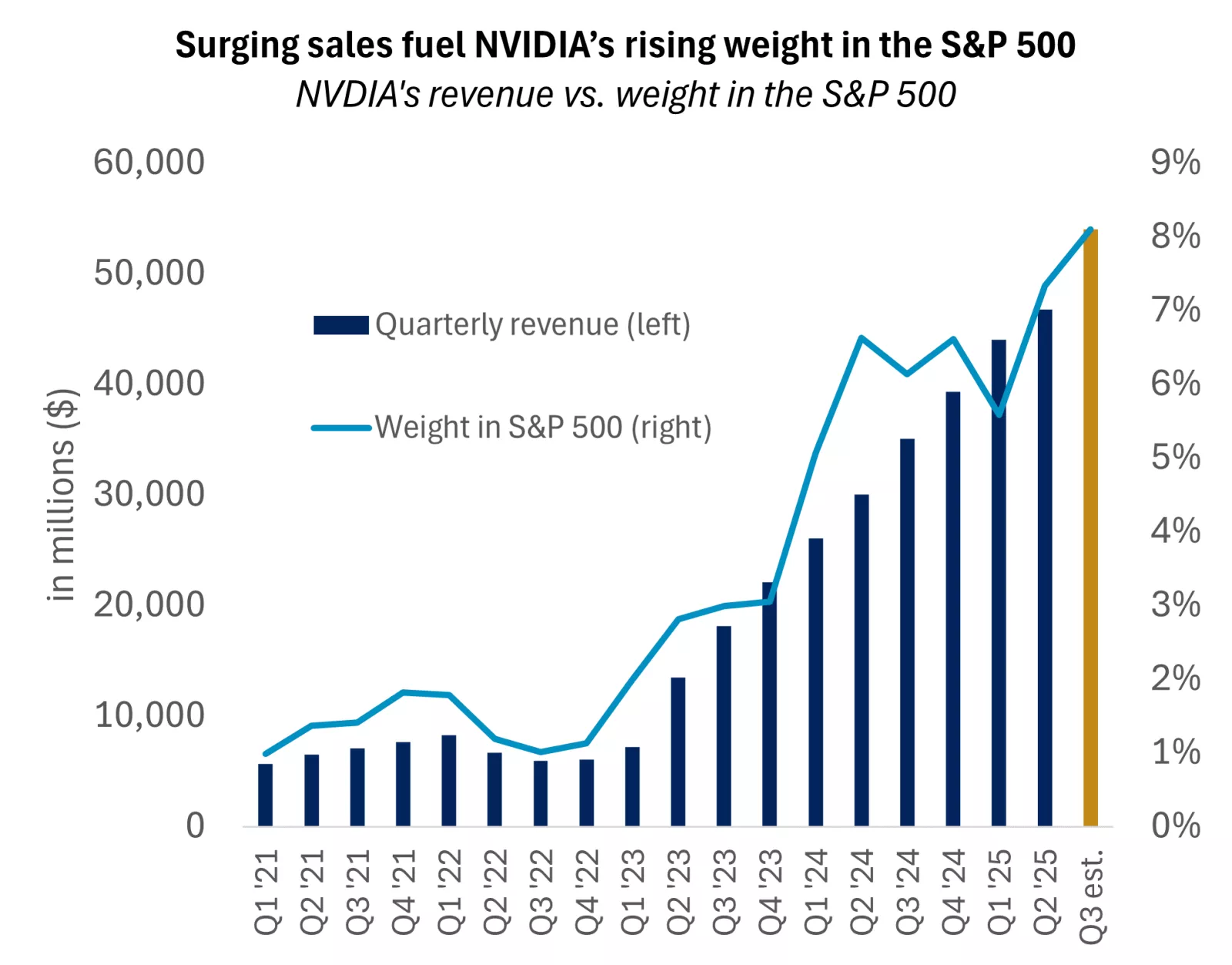

NVIDIA in the Spotlight: AI Investment’s Market Impact

Last week’s quarterly earnings report from NVIDIA—now the world’s most valuable public company, representing an extraordinary 8% of the S&P 500 by market capitalization—was a critical focal point for market participants. Despite stellar year-over-year revenue growth of 56% in the company’s second quarter (and its share price’s 35% advance in 2025), the immediate stock response was subdued. The reasons: slightly below-expected data center revenues and next quarter’s guidance that, unusually, didn’t dramatically beat consensus despite not including potential China chip sales. This muted response reflects sky-high investor expectations rather than any fundamental weakness in AI demand.

NVIDIA’s earnings reaffirmed that the AI race is still on—and rapidly accelerating. Cloud infrastructure spending by tech giants—including Amazon, Microsoft, Alphabet (Google), and Meta Platforms—has doubled to over $600 billion globally in the last two years, reflecting the race to capitalize on AI’s transformative potential. While it’s too soon to say how quickly these investments will pay off, the risk of falling behind in innovation appears to outweigh immediate cost concerns for many leading firms.

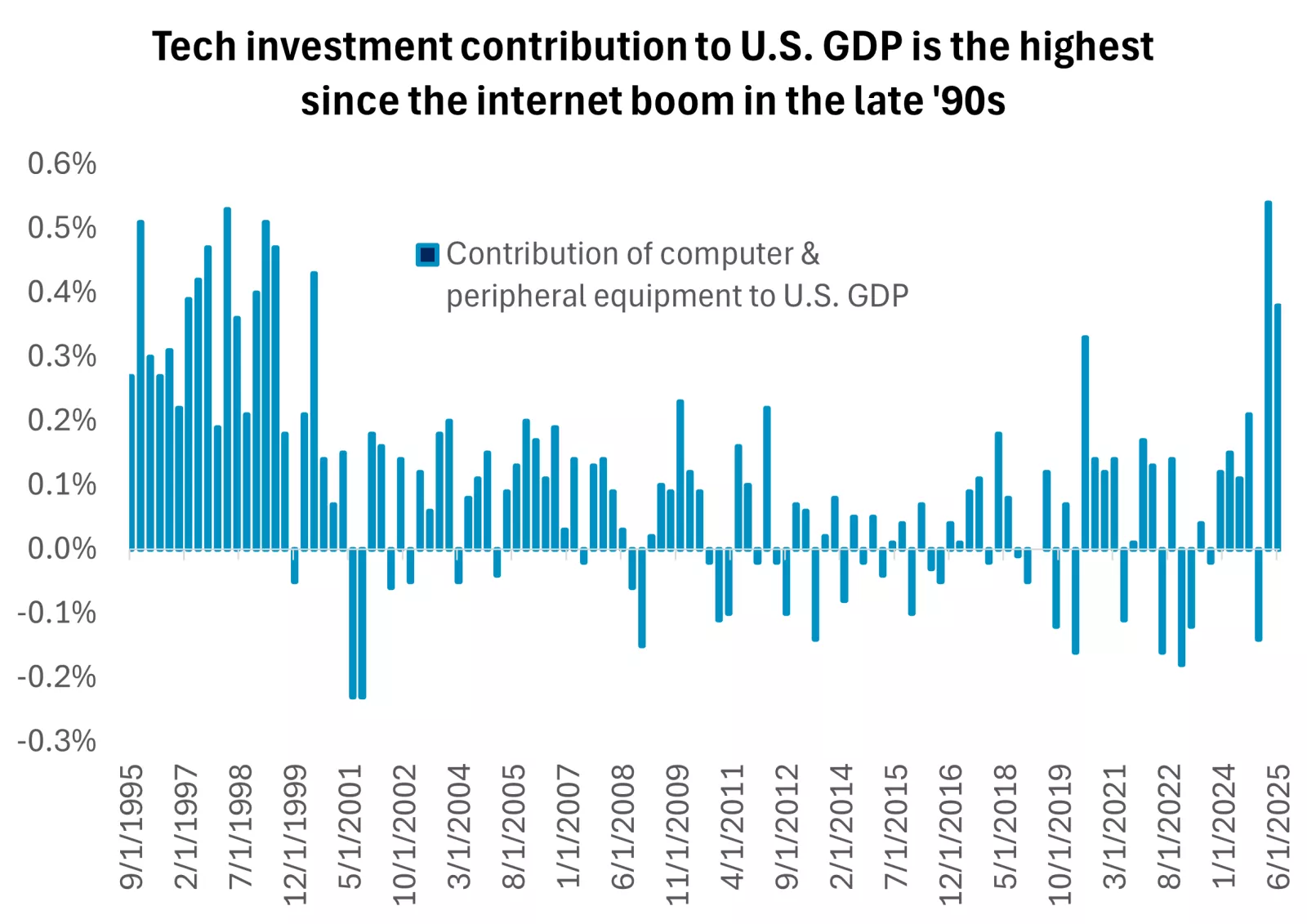

AI’s economic reach is also growing. In the second quarter, U.S. investment in computer equipment rocketed 61% annualized, while software investment soared 26%—the largest quarterly swing in over two decades. These trends, though still a fraction of U.S. GDP, are making outsized contributions and suggesting that the AI transformation is moving from narrative to measurable reality.

Broader Market Rotation as Fed Rate Cut Bets Grow

Enthusiasm for AI isn’t the sole market driver. Investor focus is now broadening as shifting signals from the Federal Reserve at its recent Jackson Hole summit have triggered a powerful rotation into previously overlooked sectors. Fed Chair Jerome Powell acknowledged growing risks in the labor market—a subtle but market-moving hint at the potential for policy easing.

Bond markets now reflect approximately an 85% expectation that the Fed will cut rates at its September 17 meeting, according to CME’s FedWatch tool and recent Bloomberg polling. This anticipation has revived interest rate-sensitive segments, with small-cap stocks climbing 7.5% in August—their best relative outperformance versus large caps in nine months. Additional gains were recorded in airline, automotive, and homebuilding stocks, while the equal-weighted S&P 500 hit all-time highs, suggesting increasingly inclusive market participation beyond mega-cap tech.

The Fed’s preferred inflation metric, core Personal Consumption Expenditure (PCE), nudged to 2.9% from 2.8% last week, matching forecasts and anchoring expectations that the Fed’s next moves will likely prioritize employment stability over more aggressive inflation-fighting. Recent Q2 GDP revisions (3.3% annualized growth, following Q1’s contraction) confirm strong economic underpinnings, further supporting the case for an accommodative monetary trajectory.

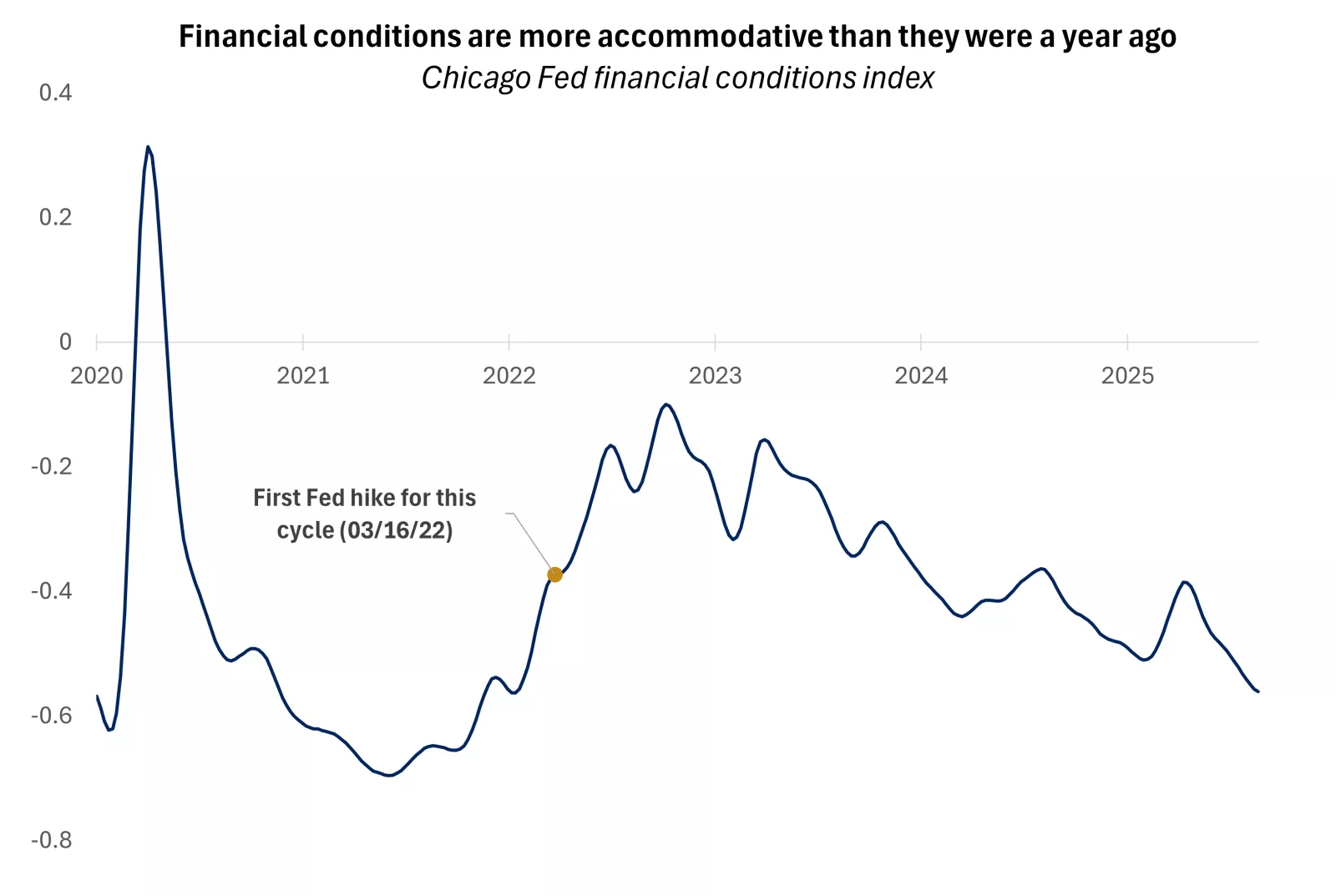

Financial Conditions: Room for Recovery—But Watch for Bubbles

Current U.S. financial conditions indices—measuring factors like interest rates, credit spreads, the dollar, and equity prices—are more accommodative than at any point since the Fed’s 2022 tightening began. Should gradual rate cuts unfold as markets expect through 2026, sectors most pressured by high borrowing costs—such as manufacturing and housing—could recover, helping broaden the rally to mid- and small-cap stocks, value equities, and cyclical sectors.

Investors, however, must remain vigilant: history has shown that extended periods of easy money can inflate speculative excess. Episodes in 2000 (tech bubble), 2007 (housing bubble), and 2021 (meme-stock surge) were all preceded by ultra-loose financial conditions. With the Fed likely to remain supportive into next year, the primary risks today are longer-term asset bubbles and, eventually, the vulnerabilities that tightening cycles inevitably unmask. For now, investors can lean into the recovery, but prudent diversification and risk management are critical.

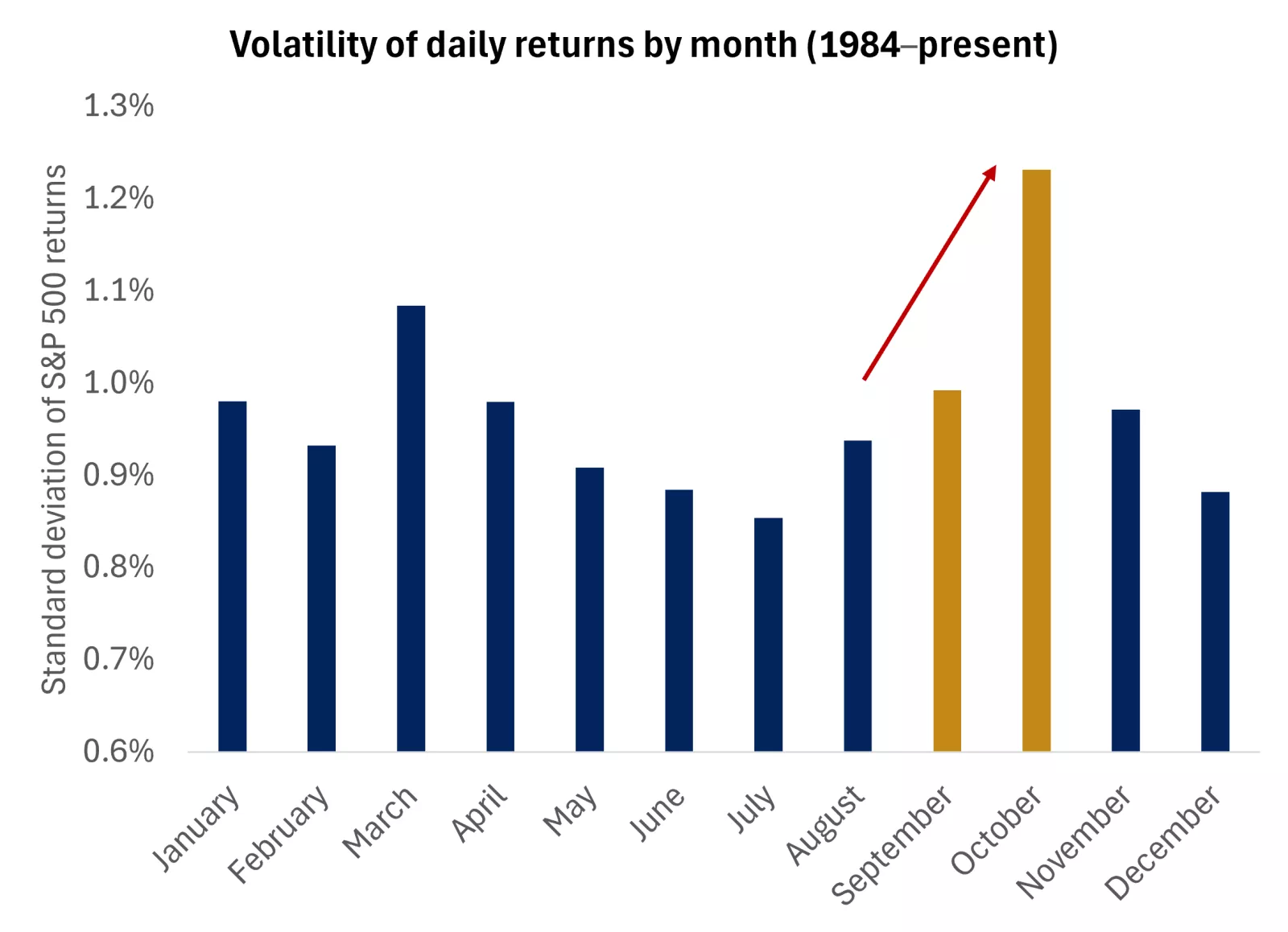

Seasonal Volatility Ahead: Maintain Diversification

Despite this positive outlook, autumn poses challenges. September and October have historically proved to be the most volatile and least rewarding months for equity investors, with the S&P 500’s standard deviation of returns rising notably. Seasonal weakness often brings short-lived corrections, but history also shows robust rebounds once the storm passes. In the current environment, where fundamental data remain strong and new leaders are emerging outside of the tech sector, seasoned investors recognize these periods can present attractive entry opportunities.

In light of recent outperformance by U.S. large caps, including many with high AI exposure, experts suggest using any autumn pullbacks to rotate into lagging mid-cap stocks, cyclical sectors (such as financials and select consumer discretionary plays), and international equities, which could help buffer portfolios against movements in the U.S. dollar. A cooling market after a record-hot summer could offer a window to rebalance and broaden investments across multiple asset classes.

Key Market Stats (as of August 29, 2025)

| Index | Close | Wk % Chg | YTD % Chg |

|---|---|---|---|

| Dow Jones Industrial Avg. | 45,545 | -0.2% | 7.1% |

| S&P 500 | 6,460 | -0.1% | 9.8% |

| NASDAQ Composite | 21,456 | -0.2% | 11.1% |

| MSCI EAFE* | 2,731 | -1.2% | 20.7% |

| 10-year Treasury Yield | 4.22% | 0.0% | 0.3% |

| Oil ($/bbl) | $64.04 | 0.6% | -10.7% |

| U.S. Aggregate Bonds | $99.46 | 0.1% | 5.1% |

Data: FactSet, 8/29/2025. Bonds represented by iShares Core U.S. Aggregate Bond ETF. *MSCI EAFE covers 4 days ending Thursday.

Looking Ahead

The upcoming week brings vital economic releases including Purchasing Managers Index (PMI) and the latest labor market reports. Investors will closely watch these for further insights into the Fed’s rate-cut calculus and the underlying strength of the U.S. economy.

As seasons change, disciplined and diversified investing remains imperative. The summer’s AI-driven sizzle may cool, but fundamentals and broader market participation set the stage for a resilient second half of the year.

{kind=link}