Weekly Market Wrap: Fed’s Rate Cut Kicks Off New Easing Cycle

Published: September 19, 2025

Fed Resumes Easing Amid Labor Market Jitters

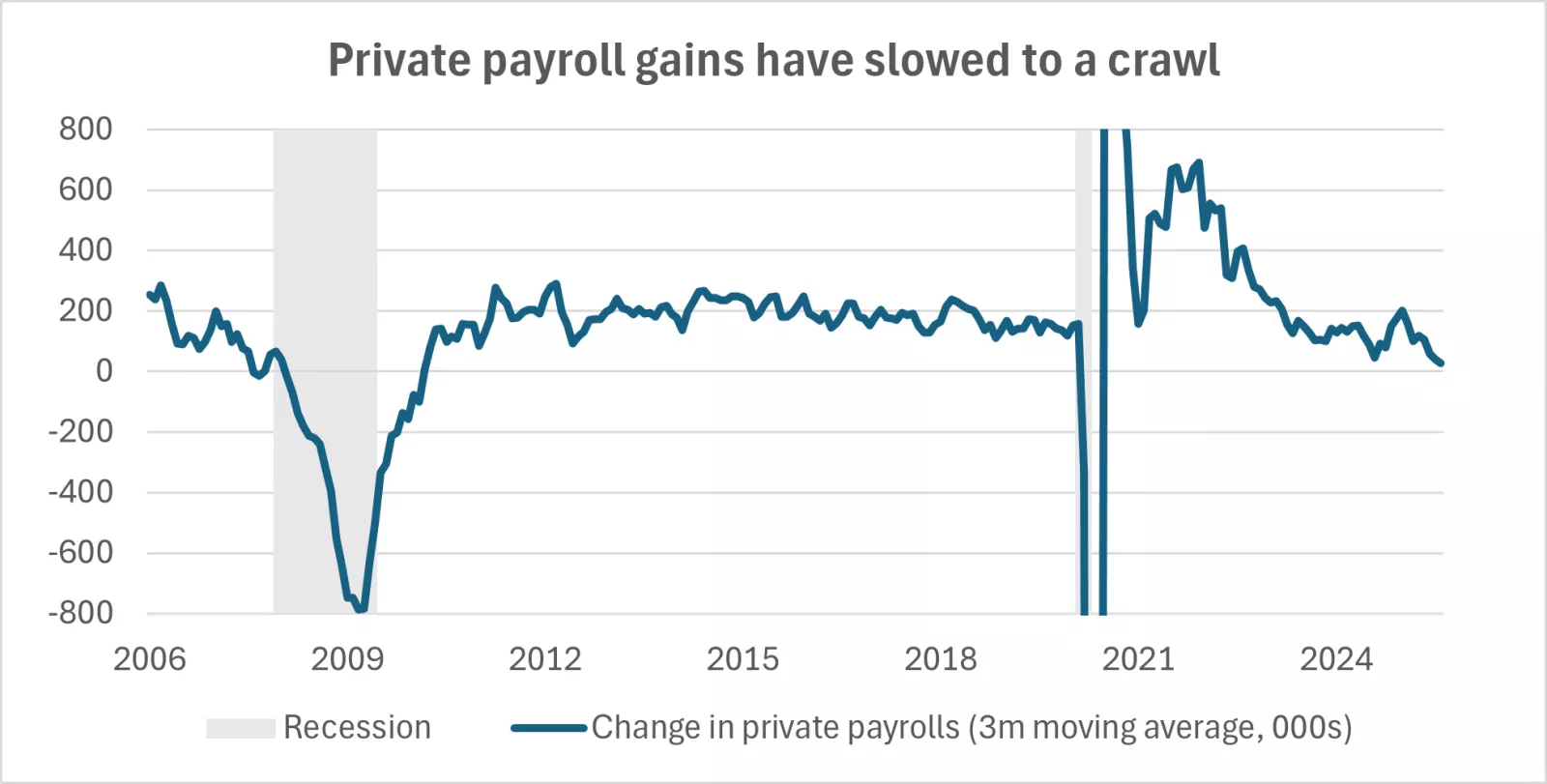

The U.S. Federal Reserve has resumed its rate-cutting cycle, implementing its first policy reduction of 2025—a 25 basis point (0.25%) cut—after nearly a year on hold. The move was widely anticipated by market participants and signaled a proactive approach by the central bank to buffer the U.S. economy against signs of a wavering labor market. This action comes as private nonfarm payroll growth has slowed considerably, prompting concerns about the sustainability of the expansion and the risk of recessionary forces gaining traction.

Recent labor data highlighted that the average pace of private sector job additions has decelerated to just 29,000 per month, a level previously observed only around economic downturns or recessionary onsets. The number of job openings has also slipped below the count of unemployed Americans—a dynamic not seen in nearly a decade, excluding the pandemic period. The unemployment rate has shown a modest, but persistent, upward drift.

However, some analysts note these trends are partially attributable to declining net migration, and companies, despite slower hiring, are not increasing layoffs at alarming rates. Meanwhile, economic growth remains resilient, with the Atlanta Fed tracking third-quarter GDP at an annualized 3.3%, buoyed by steady consumer spending.

Ambiguity on Future Fed Moves Raises Market Uncertainty

While the decision to cut rates was nearly unanimous among Federal Open Market Committee (FOMC) members, projections for future policy are anything but clear. The FOMC’s so-called “dot plot,” illustrating policymakers’ individual outlooks, reveals significant disparities. The median expectation suggests as many as two more 25 basis point cuts are possible by year-end, but 40% of FOMC members forecast no further easing at the remaining 2025 meetings. Looking further out, views diverge widely on where rates will settle by late 2026, ranging from 2.75% to 4%.

During a post-meeting press conference, Fed Chair Jerome Powell emphasized that future decisions would depend on incoming data, reflecting the complexity of balancing inflation risks with mounting signs of labor-market weakness. Market participants now face extended periods of speculation and elevated volatility around each major economic data release, particularly on jobs, inflation, and growth.

Market Reaction: Rallies and Rotations

Equity markets responded positively to the rate cut and the prospect of more accommodative policy. Rate-sensitive segments, notably small-caps, outperformed: the Russell 2000 Index surged 8.3% over the past month to a record high, outpacing the S&P 500 and Nasdaq. This reflects optimism that easier financial conditions and anticipated fiscal policy support—including expected tax cuts for 2026—will bolster corporate profits and economic momentum.

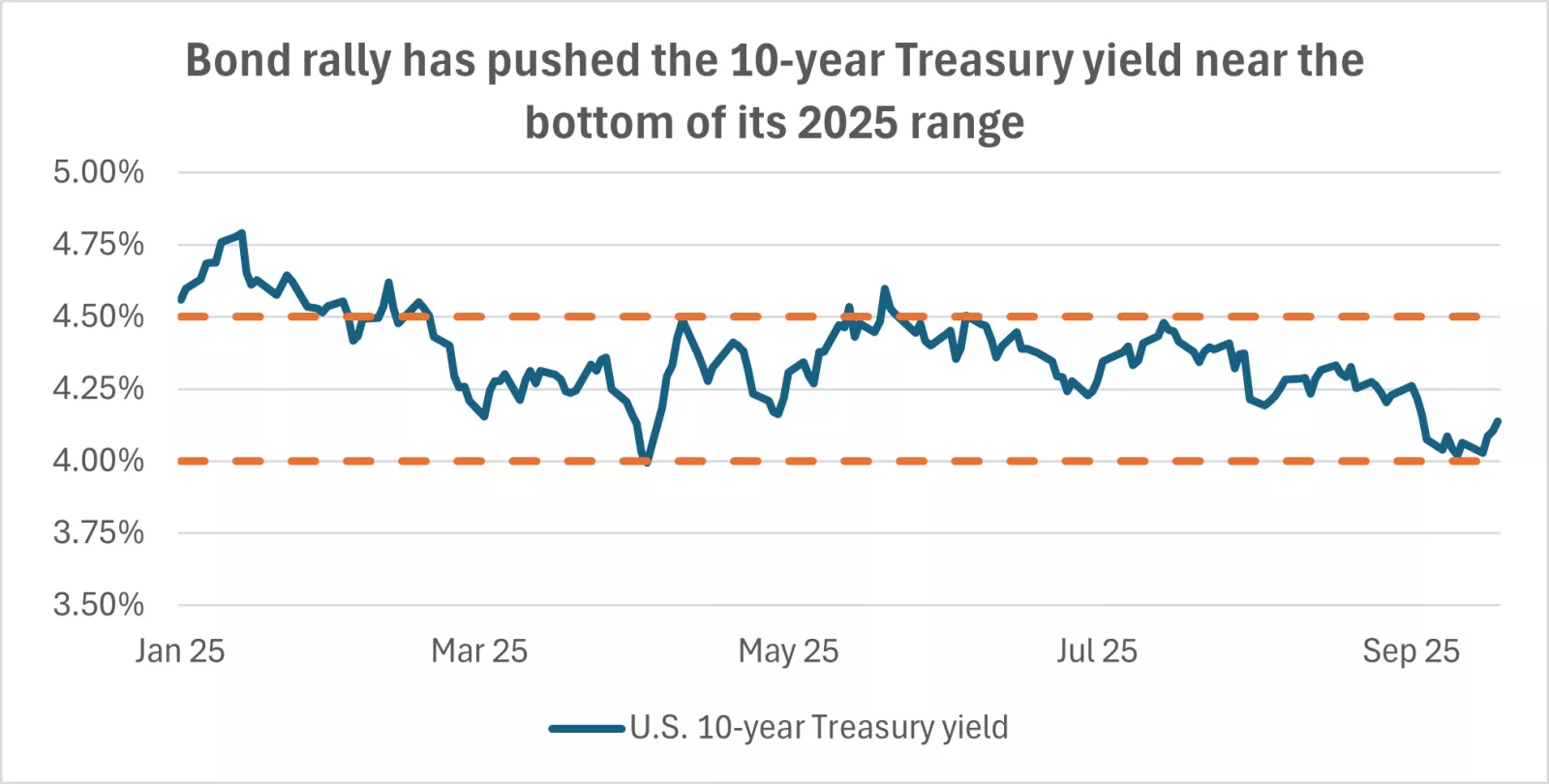

On the fixed income front, the rapid repricing of rate expectations fueled a rally in U.S. Treasuries, bringing the 10-year yield down to the lower end of the anticipated 4%-4.5% range. However, with so much optimism now priced in, strategists are turning cautious on extending bond portfolio duration, mindful not only of inflation risks but also potential fiscal pressures that could push yields higher.

Market-implied probabilities suggest over a 90% chance of rate cuts at both upcoming Fed meetings in October and December, although these bets could be challenged if labor data rebounds or inflation unexpectedly accelerates. For now, U.S. equities remain favored, particularly large- and mid-cap names across consumer discretionary, financials, and health care sectors.

Investment Strategy: Caution Amid Opportunity

The ongoing shift in U.S. monetary policy means investors must remain alert to both opportunities and risks. While lower rates and fiscal expansion are likely to support growth, the ambiguity surrounding the Fed’s path, volatile global macro conditions—including subsiding but still-present trade friction, and ongoing geopolitical risks—suggest that market swings may intensify.

- Maintain a preference for U.S. large- and mid-cap equities, with an eye toward quality and cyclicals poised to benefit from easier conditions.

- Reassess fixed income duration exposure as much of the near-term positive reaction in Treasuries appears priced in.

- Monitor key economic releases—including labor reports, PCE inflation, and consumer sentiment—for fresh signals that may shift Fed expectations and market sentiment.

- Consider the benefits of diversification, while acknowledging that volatility and noisy data could create tactical opportunities and risks alike.

Weekly Market Statistics (as of September 19, 2025)

| Index | Close | Week | YTD |

|---|---|---|---|

| Dow Jones Industrial Average | 46,315 | 1.0% | 8.9% |

| S&P 500 Index | 6,664 | 1.2% | 13.3% |

| NASDAQ | 22,631 | 2.2% | 17.2% |

| MSCI EAFE | 2,760 | 0.0% | 22.0% |

| 10-yr Treasury Yield | 4.13% | 0.1% | 0.2% |

| Oil ($/bbl) | 62.36 | -0.5% | -13.1% |

| Bonds | $100.29 | -0.2% | 6.2% |

Source: FactSet, Edward Jones, as of September 19, 2025. Bonds represented by the iShares Core U.S. Aggregate Bond ETF. Past performance does not guarantee future results. MSCI EAFE data represent four-day performance ending Thursday.

Looking Ahead

Investors and analysts will watch a comprehensive slate of economic reports this week, including updates on PCE inflation, consumer trends, housing sector data, GDP growth estimates, and purchasing managers’ indexes. These indicators are likely to play a key role in shaping expectations for monetary policy and capital flows as Q4 approaches.

This Weekly Market Wrap is for informational purposes only and does not constitute specific investment advice. Market conditions and investment opportunities change frequently; consult your financial advisor for guidance tailored to your situation.

{kind=link}